What the Eurozone Means for Irish Economy

|

Since 1999, and the introduction of the currency, Ireland has adopted the Euro as its currency of choice. Along with the obvious benefits of improving trade possibilities for our economy, and improving travel opportunities for our inhabitants, this currency union has many drawbacks. These drawbacks centre around the loss of control of monetary policy. The issue this posed manifested itself most clearly in the lead up to the crisis of 2008; for q3 to q4 2007, real GDP grew in Ireland by 4.5% and by only 0.49% in the Euro area. Similarly, Irish inflation in 2007 averaged 4.9%, whilst in the Euro area inflation was at 2.45%, a level far closer to the usual ECB target of 2%. At this time the ECB deposit rate was 3%, arguably far below the optimum level that would have been required to dampen the Irish Economy.

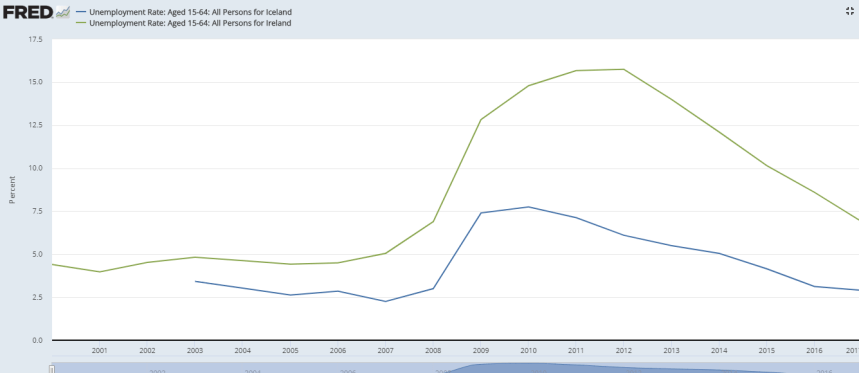

Having examined the missed dampening opportunities, consider the monetary response to the Irish crash, specifically in comparison to a country of similar conditions but independent monetary policy; Iceland. Due to its astronomical level of privatised bank debt pre-global financial crisis, Iceland experienced an economic downturn of epic proportions in 2008. Per Capita GDP had fallen by 26.9% at the height of the crisis, in comparison to a drop of 14.9% in Ireland, however unemployment increased by a far greater percentage in Ireland and was more prolonged. Iceland managed this mitigation of negative outcomes through a dramatic devaluation of their currency, thus inciting a trade surplus by making Icelandic goods relatively cheap to foreign buyers, and reducing the cost to Iceland of foreign debt interest payments.

As Ireland was locked into a currency union with countries not going through downturns of the same magnitude, monetary policy such as this could not be implemented. As a result, the Irish economy took many years more to recover from its downturn and felt effects which were exacerbated by mismatched interest rates imposed by the ECB. Leaving the European Monetary Union does not imply a departure from the EU, rather it suggests the implementation of a structure similar to the UK’s pre-Brexit relationship. This still allows for movement of people and money, along with maintenance of the Customs Union. From a regulatory perspective, no changes would be made to current trade and travel arrangements with the EU. However a departure from the Eurozone would imply poorer EU relations. The current view of the Eurozone is that it is a long term investment. One which will see favorable returns when all participating economies are closely developed and interlinked on a level playing field. However like all investments, return is not guaranteed. |

Test test

LikeLike