Creative Destruction: Gaining in strength?

Perhaps one of Schumpeter’s most revered theories is that of creative destruction. His argument that capitalism never stands still, with long-standing, inefficient processes decaying in the wake of newer, superior ones has stood the test of time well, and in the aftermath of a global pandemic, appears to continue in this light.

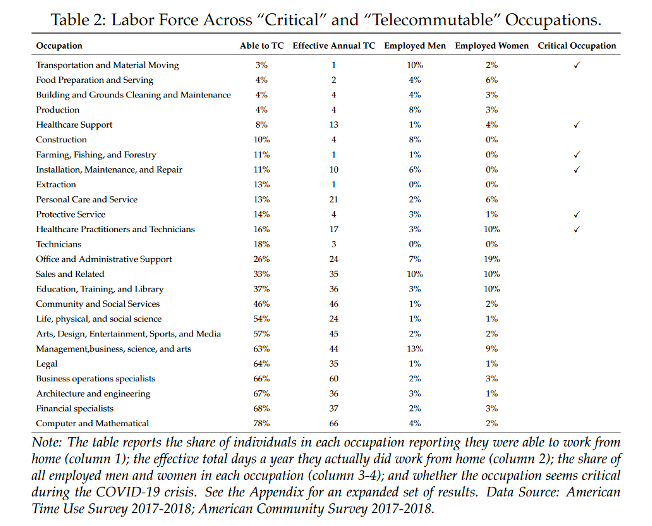

WFH – a trend, an improvement, or both?

A more obvious impact of the pandemic-induced lockdowns was the ‘Work From Home (WFH)’ situation, which many workers and students found themselves in. While evidence suggests that students and young graduates certainly wish for a return to an in-person normality, the technology, flexibility and heightened global interconnection that accompanied this WFH trend can be seen as a form of creative destruction. This is due to the replacement of older, less efficient, less flexible practices undertaken by offices with more productive, collaborative ones. With meeting participation increasing by over 2900% over the course of the Pandemic, the rise of Zoom neatly epitomises this creative destruction. Existing for almost a decade prior to the pandemic, Zoom’s overtaking of Skype, and other lower quality, more complicated platforms, coupled with a rise in global interconnectivity from which it prospered, illustrates that the foundations for creative destruction had been in place. However, it was the catalyst of the Pandemic that fuelled the eventual ousting of these inefficient processes.

Miracle Advances in Healthcare

Being a crisis in healthcare, the impacts of Covid-19 on the sector were always going to be large. As the world locked down, the personal profit from vaccines became huge, with many viewing vaccine development as the only sustainable way out of the crisis. Furthermore, for big pharma businesses, net profits from development were promising, as BioNtech’s expected revenues of €15.9 billion for this year illustrate. Thus, the fastest vaccine development in history (previously held by the mumps vaccine, which took four years to develop) followed, hailing what scientists proclaim as a new era of vaccine research. Much like the Work from Home technology, the knowledge of mRNA, alongside the ability to accelerate the testing and approval processes had been around for decades, yet a lack of funding and cooperation meant that such techniques and pace never came to fruition. Thus, the catalyst of a global pandemic rendered inefficient processes useless, in favour of more productive research techniques. While admittedly this research was far better funded than in the past, the lessons learned within the immunisation research sector, alongside the new-found ability to produce vaccines at such pace, and with new techniques, means that the creative destruction ought to last within the industry. This should heighten the efficiency and productivity of future research.

Similarly, the speed of drug development processes to aid those seriously ill with Covid-19 underwent rapid increases during the pandemic. Like with the vaccines, much of this came from the regulation-side, with approval and testing processes being fast-tracked, and the removal of unnecessary paperwork (recognised as inefficiency-inducing ‘sludge’) aiding this. Additionally, cooperation and parallel experimentation again played its part in heightening efficiency in the sector, a rise in productive techniques that many scientific researchers think will remain in a post-Covid world, further illustrating the impact of the pandemic on inducing creative destruction.

Online Shopping’s Anticipated Breakthrough

Where the biggest acceleration (rather than initiation) of creative destruction can be seen is in the retail sector, as many began relying solely on online shopping for everything from food to clothes to newspapers. Additionally, HSBC’s UK head of network noted that the closure of eighty-two of their branches between April and September 2021 was a result of the trends away from branch banking that were underlying pre-Coronavirus, with a decrease in footfall by a third in the last five years, and 90% of contact being completed remotely. This illustrates direct creative destruction at work in the retail banking sector. Furthermore, this shift to online shopping and banking has increased price and competitor transparency, meaning that allocative efficiency has heightened, bringing the market closer to its societal equilibrium, and meaning that firms must react to market trends to remain competitive – therefore increasing the sustainability of this creative destruction into the future.

Key Take-Aways

The above processes illustrate creative destruction at work, reacting to the shock event of a global pandemic. The requirement in this instance of an event – Covid-19 – to accelerate, or even to consolidate and finalise this creative cycle could signal that Capitalism’s competitive processes were existent, yet running slow prior to the Pandemic. Taking a wider view, the extension of creative destruction to the public sector, notably with the impacts on healthcare and administrative/bureaucratic processes, ought to introduce a healthy level of heightened innovation and competition to sectors where this has previously been lacking. Whether the impacts of Covid-19 on heightened efficiency here will last remains to be seen, not-least for some areas of clinical research have been negatively impacted by the disruption of the Pandemic, yet many researchers, notably within immunology and drug development, are confident that the streamlined and productive lessons learned will be here to stay.

Furthermore, the sudden requirement for private firms to react and innovate, not only to compete, but in this case to stay financially viable means that lasting effects on firms includes an obligation to be sustainably efficient and inventive, with a new focus on pro-activity rather than re-activity to the next crisis, in order to remain profitable.